Since the World Health Organization announced that COVID-19 had become a pandemic, there has been gross economic fall out all over the world. In Canada, large and small businesses have temporarily closed, leaving many employees no longer working or drastically reducing their productivity, and many people have been laid off, such as those on a contract or paid by the hour. The unemployment rate, while in this quarantine and self-isolation period, can be compared to that of a great depression since it now easily exceeds 20 percent of the population. According to Canadian Federation of Independent Business, it expects 25% of businesses won't be able to survive a one month closure. In Canada, it's also not a secret that most people pay a large part of their monthly income towards mortgage debt. Ironically, even before the Coronavirus pandemic, Canadians had a significant problem concerning affordability in cities like Toronto, Greater Toronto Area and Vancouver. Payment shock - where a rise in interest rates causes sudden mortgage default - was a paramount issue addressed continuously by the Government, which led to the stark implementation of the Mortgage Stress Test, foreign investment tax and changes to insurable mortgages, for example. These measures were meant to bring down overheating in the real estate market. The idea that a better global economy, with the need for rising interest rates, could push borrowers into insolvency never materialized—quite the contrary. Instead, the insolvency and default risk is now from a virus, and it's ravaging the economy at an accelerated and unprecedented speed. For mortgage borrowers, the fear of default is now front and centre and figuring out what the consequences mean is a top priority for Canadians. In a typical scenario of mortgage default due to economic changes and a rise in interest rates, a lender can enforce remedial measures such as foreclosure or power of sale, which would allow it to take possession of the property and resell it to recover any potential losses. Fortunately, during this time of uncertainty where default is likely inevitable, banks and other financial institutions like those accessed through the broker channel, are working closely with mortgage borrowers to eliminate any financial risks in the near future. By using a well-known mortgage privilege called "Skip a payment" and "Defer A Payment," borrowers can make comfortable arrangements with their lender to manage the next couple of months. Explained, deferring or skipping a payment means paying a mortgage later. The mortgage payment does not get waived. Instead, it is delayed and usually added to the end of the mortgage loan. Additionally, interest usually still accumulates from the date of deferral, and so its important borrowers speak to their lender to ensure they understand the total cost involved in deferral. Concerning the Coronavirus, to be eligible for mortgage deferral, a person must be in quarantine due to possibly having or being diagnosed with Coronavirus or must have been laid off from their employer due to Coronavirus concerns. Keep in mind, each lender has its specific criteria and borrowers should call their respective mortgage lenders to ensure they fit the criteria and to commence or schedule deferring their payments. Generally speaking, mortgage lenders offer deferral in situations where a person has become unemployed or experience a significant financial setback, so exercising this option because of the Coronavirus is entirely natural. Most lenders always offer the ability to pause a mortgage or take a "payment vacation" for unexpected situations. Exercising these options, if approved by the mortgage lender, will not have a negative impact on a person's credit or the ability to renew or refinance their mortgage. If you require help navigating this process, please do not hesitate to call or write. Sarah A. Colucci Mortgage Agent Lic. M14000929 Mortgage Edge, Broker 10680 Direct: (647) 773-4849 Email: sarah.colucci@mortgageedge.ca

2 Comments

During the next few months and maybe even longer, depending on the extent of the economic damage caused by COVID-19, Canadian mortgage borrowers may find themselves in difficult financial circumstances, which may make mortgage payments impossible. During the annual march break up to April 5th, most services in Ontario have closed. Many employers, professional colleges, and unions have also taken steps to encourage employees to work from home by closing corporate offices and suspending routine medical visits. Some people are staying home without pay, while those currently with pay may soon find it eliminated during this unprecedented time of minimal social interaction and retreat and unemployment. Luckily, the Canadian Government has put together a stimulus package that includes Employment Insurance and necessary relief for those who will not be receiving their regular salary now or in the near future. Additionally, CMHC has offered relief for those in high-ratio or insured mortgages. An insured mortgage is a type of loan (usually taken out on a purchase transaction) that involved a downpayment of 19 percent or less and where an insurance premium was charged or a mortgage through a Mortgage Finance Company, for example. If you are unable to pay your insured mortgage because of unemployment, I can help find you the right solution. I will work with CMHC on your behalf. For all mortgages insured by Canada Mortgage and Housing Corporation (CMHC), we can take the following approaches:

If none of these solutions work, CMHC is willing to consider other alternatives I present to them that make sense. As always, if you'd like to learn more, please do not hesitate to call or write. Sarah A. Colucci Mortgage Agent Lic. M14000929 Mortgage Edge, Broker 10680 Direct: (647) 773-4849 Email: sarah.colucci@coluccimortgage.com  Are you now considering trading in your current mortgage for a better rate?

Borrowers usually refinance their mortgage to consolidate debt or access the equity in their home. Yet, during times in the market when interest rates plunge like the situation we are now experiencing with COVID-19 and the global economy, borrowers may likely seek the opportunity to trade their current mortgage rate for a lower one to save money. Depending on what the pre-payment penalty is and the difference between the current interest rate and new interest rate, it may be an excellent opportunity to trade mortgage rates, which can save tens of thousands of dollars within the next mortgage term, and of course, over the life of any mortgage. Let's look at what trading a $400,000 mortgage at 3.99 per cent for the same balance at 2.59 per cent means in terms of total savings. Scenario A Current Mortgage Balance $400,000 Interest Rate: 3.99% Amortization Period: 25 years Monthly Payment: $2,101.91 Total Interest Payments in 3 years: $45,797.95 Scenario B Mortgage Balance $400,000 Traded Interest Rate: 2.59% Amortization Period: 25 years Monthly Payment: $1,809.34 Total Interest Payments in 3 Years: $34,213.53 In the above scenarios, it is clear that a borrower saves a lot of money in two different ways. First, their monthly payment is reduced by $292.57 and second, they save over $11,583.47 in interest payments in just three years. Of course, total interest savings may fluctuate depending on the length of time remaining in the mortgage term and the mortgage balance; however, the fact remains that trading for a lower interest rate can have significant financial advantages. Also, a borrower may end up with a lower rate mortgage for an extra two years, if interest rates rise after their original mortgage matures, which would save them an additional two years of extra interest payments. This could easily be more than $10,000 worth of savings. In this case, at the end of the five years, the total savings could be approximately $21,000 or more! If you're contemplating refinancing today by trading your current interest rate for a lower one, you need to determine your pre-payment penalty and then how much money refinancing your mortgage actually saves you. I usually complete this activity with my clients over the phone, so it makes "running the numbers" a convenient experience. Are you interested in learning how much you can save by refinancing your mortgage for a lower rate? Please don't hesitate to call or write. Sarah A. Colucci Mortgage Agent Mortgage Edge, Broker 10680 Direct: (647) 773-4849 Email: sarah.colucci@coluccimortgage.com  Refinancing your mortgage can help you save tons of money - and not just immediately but also over the rest of your mortgage term, too. I'm not just saying this, either - it's VERY TRUE.

One of the reasons homeowners do not refinance is they believe it may be too costly, the process too lengthy, or they may have to pay a higher interest rate, which defeats the purpose of renegotiating their mortgage. There are also other reasons homeowners do not refinance, which also make up a part of the myths about refinancing floating around today. Unfortunately, misinformation can often get in the way of homeowners saving money and getting their financial profile in a better position. The truth is by renegotiating a mortgage contract through refinancing; a person CAN free up a significant amount of cash flow and also pay LESS interest on their outstanding debts. Refinancing, therefore, can be (and often IS) a big win for anyone looking to save money. The process is also not lengthy and can get completed as soon as one to two weeks from the date of application. Costs Some borrowers have a hard time crunching the numbers and determining how much they can save from refinancing. In this case, it is essential to consider two realities. First, a borrower usually refinances into a lower rate mortgage and consolidates high-interest debt like credit cards or unsecured personal loans. This means that over the next term of their mortgage, they save tens of thousands of dollars in interest payments because they traded higher interest for low interest and eliminated disastrous interest-only payments on other credit. Paying less interest to the banks also means more principal gets paid against their mortgage loan, which means MORE SAVINGS and hopefully, more money in the bank over time. Most people cringe when they learn how much money they've been blowing on a monthly and yearly basis on credit card balances that don't go away. They are shocked when they learn how credit card companies calculate interest and how the odds are against them when it comes to paying off their balances. What happens if mortgage rates go higher? If the proposed mortgage interest rate is higher than the actual rate, then it is essential to look at WHY one is refinancing in the first place. If someone is drowning in monthly debt payments, which consist of interest only, meaning they will NEVER pay their balances off in full, then a mortgage with a higher rate remains a great option. In the case of interest rates, it is critical to realize that no one has been able to time the market and interest rates with 100 percent accuracy. Waiting for interest rates to decline may be a losing battle because, during the wait, the interest rates may climb even higher. Running the numbers and determining total savings is the gold standard at proving whether refinancing is a viable and worthwhile option or not. Only after running the necessary calculations and examining the savings can a person make sound decisions. Are banks the only place you can refinance your mortgage? Major banks are just one type of lender - there are more. Mortgage finance companies accessed through the broker channel and credit unions, for example, can offer much better deals at any given time. Most people are programmed to believe that banks are the best place to get mortgage financing. Depending on the type of borrower, credit, and income, a borrower may be better suited for a different kind of lender, which is why it is worth exploring different options. A mortgage broker can help you shop around, which increases your chances of finding the absolute best deal on your mortgage. Refinancing - not the only answer? Sometimes after running the numbers refinancing is not the best option. The prepayment penalty may be too costly, and the person should stay where they are. At this point, we must ask: Are there other options? The good news is YES. A borrower in this situation - one where they shouldn't touch their first mortgage, can explore a second mortgage, line of credit or private loan. Private loans, contrary to popular belief, do not cause financial hardship. They can be a great way to put a "bandaid" on a situation temporarily while some other situation sorts itself out. There are many different reasons a person may require a private loan, and if refinancing is out the question, a borrower should speak to their mortgage broker about getting this type of loan and pricing, and so on. Do you have mortgage questions? Please feel free to call or write. Sarah A. Colucci Mortgage Agent Mortgage Edge, Broker 10680 Direct: (647). 773-4849 Email: sarah.colucci@coluccimortgage.com  A mortgage is a contract between a borrower and a lender. A mortgage is usually "closed" for a certain length of time. In Canada, mortgage terms can be as short as one year or as long as ten years. There are some "open" mortgage products, such as a line of credit that offer borrowers more flexibility to prepay with the ability to exit at any time. I explore these at the end of this article.

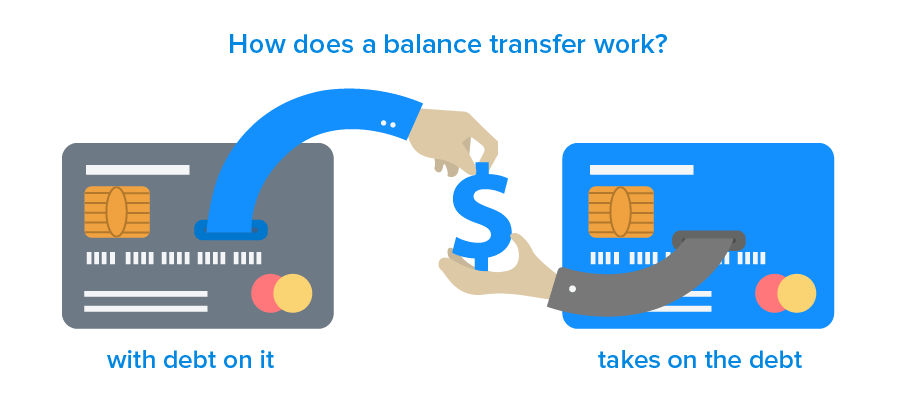

Closed mortgage products are locked in, and a borrower who enters a closed mortgage product promises to uphold their agreement for the length of the entire term. If a borrower decides to break their mortgage contract or "break their mortgage" before this time, they have to pay a pre-payment penalty. The amount they pay depends on how much time remains in their term along with the type of interest rate they have, such as a fixed or variable rate. In a variable rate mortgage, the penalty is usually just three months' worth of interest regardless of how much time remains. A fixed-rate mortgage, on the other hand, gets calculated using the Interest Rate Differential or three months' worth of interest, whichever is greater. Perhaps one of the most significant deterrents of refinancing for most people is having to pay a pre-payment penalty. Most people are afraid to ask what the penalty is and feel the burden of the costs associated with renegotiating their mortgage does not outweigh the benefit of refinancing. Here are some things to think about: Blend and Extend Sometimes, a borrower can avoid paying the penalty in a refinance situation if they stay with the same lender. Most lenders can increase the amount of mortgage, and blend the old rate on the previous loan with the new interest rate on the additional funds requested. The time left remaining in the term stays the same, which means there is no penalty. So, for example, a mortgage of $400,000 can be increased to $500,000 with the same financial institution, and the old rate of let's say 2.99 percent on the $400,000 gets blended with the new rate of 2.59 percent on the $100,000 requested. Therefore, the total new rate on the new blended mortgage amount of $500,000 is 2.79 percent, for example. The remaining time left in the term of the mortgage stays the same and therefore, there is no penalty. Considering The Costs Of A Penalty. Although most refinances trigger a penalty, it's essential to consider the benefits and risks and calculate whether the savings outweigh the penalty incurred. If a borrower has substantial unsecured credit card debt, for example, then paying the penalty may be wiser than continuing to make interest-only payments on never-ending credit card balances. For example, a borrower may pay over $4,000 in minimum payments to creditors each year, which over time, can add up to significant financial losses. Meanwhile, paying only a one-time $3,500 penalty may make more sense than continuing to pay interest-only on credit cards since, over time, principal owning on the mortgage debt gets paid down in addition to substantially lower interest on the entire balance. Compare mortgage rates to 23.9999% credit card interest. In three years, the credit cards would have absorbed approximately $12,000 in interest-only payments, and the actual balances of those cards wouldn't have been reduced. Therefore, paying the penalty, in this case, is well worth it. Line of Credit There is one other way to avoid paying mortgage penalties, which is considering an "open" mortgage product like a line of credit. An open mortgage product does not cost money to leave and can be prepaid at any time. A line of credit can get registered in "second" position, which means the existing first mortgage does not have to get broken or renegotiated. Meridian Credit Union and Manulife Financial, for example, both offer secured lines of credit (in the second position) exclusively through the broker channel to all applicable borrowers. If a borrower does not qualify, we also offer the Equityline Visa, which is perfect for those with bruised credit or not enough confirmable income, such as limited self-employed claimed income, for example. In the alternative, a borrower should also explore a total equity plan which combines a closed first mortgage with a secured line of credit, both at competitive interest rates. Do you require some financial restructuring? I am specialized in money-management and choosing optimal mortgage financing products. Call or write today. Sarah A. Colucci Mortgage Agent Lic. M14000929 Mortgage Edge, Broker 10680 Direct: (647) 773-4849 Email: sarah.colucci@coluccimortgage.com ** Our high-ratio mortgage rates are as low as 2.44% for a five-year fixed rate. Refinances as low as 2.59%. Conditions apply. Call or write for details.  If you're an aspiring first time home buyer, you may have many questions about the buying process. From getting a pre-approval to understanding your mortgage terms to closing your purchase transaction with your lawyer - it can feel like too much information to absorb! In this article, I will explain the mortgage process involved in buying your first home, including Pre-Approvals, Mortgage Approvals and Lawyer and Closing. 1. Pre-Approvals. Once you have decided that it's time to purchase your first home, you'll need to figure out your budget. This means you have to determine how much you can afford and how much mortgage you can qualify for. A pre-approval is very different from a pre-qualification that most people conduct online. A pre-qualification is based on an embedded online calculator that uses your current income and your available down payment against basic mortgage qualifying guidelines. It doesn't take into account different lending products that may be available like the ones that accept the child tax credit or can gross up self-employment income, for example. Therefore, the results of a "pre-qualification" are very generic and will not provide you with precisely what you are looking for in terms of concrete approval figures. When you are about to spend your precious time shopping for a home, you must know the facts about what you can purchase instead of relying on generalities or gross assumptions. The better prepared you are, the easier the process will be! A certified pre-approval, on the other hand, involves an authentic and detailed mortgage process that verifies every aspect of your application to ensure you qualify for a mortgage. It also provides you with extremely accurate numbers, which significantly improve your chances of purchasing your dream home. If you had to compete with a purchaser, it helps to have the capacity to be able to make a strong offer. Additionally, you can focus on price points you know you can afford, which saves time and energy. A pre-approval can also hold an interest rate for you for up to 120 days, which protects you with a low-interest rate for an extended period. Getting a pre-approval is a straightforward process. During a consultation, you will be asked for your employment documentation, down payment verification and your personal information such as social insurance number, date of birth, current address, and so on. For a list of the type of documentation you will need to verify your employment, please click HERE. If you'd like to make an appointment to discuss obtaining a pre-approval, please call 647-773-4849. A pre-approval consultation provides you with an opportunity to discuss different mortgage products and whether to take a shorter or longer-term or choose a fixed or variable rate product. 2. Mortgage Approval Once your offer has been accepted, your real estate agent should send the Agreement of Purchase and Sale together with the MLS Listing to your mortgage professional. Since the pre-approval was already conducted, and you already provided the relevant documentation upfront, the process of mortgage approval should be relatively straightforward from this point onward. Your mortgage agent or mortgage advisor will submit your official mortgage application to the lender of choice and forward you the approval documents to sign electronically (since most lenders accept electronic signature) or in person, once approved. At this point, you can confirm your mortgage payments, interest rate, mortgage terms like pre-payment privileges and double up options and also ask any additional questions you may have about the financing and closing process. 3. Lawyer and Closing Once you have accepted your new mortgage terms and signed all the necessary documentation, your mortgage lender will instruct your real estate lawyer. Mortgage instructions are a set of documents directed to your lawyer indicating how the bank would like him or her to register your mortgage on title to your new property. You will often find that, in addition to legal and title documents you will be asked to sign, you will also be required to sign the original mortgage documents again. This activity provides you with a second opportunity to go over the original mortgage commitment to ensure you understand all of the terms. Once everything is signed, and your closing date approaches, your mortgage lender will wire transfer or direct deposit the mortgage funds into your lawyer's trust account. With the mortgage proceeds and your remaining downpayment (less your deposit with your offer), your lawyer will provide the seller's lawyer with the funds required to close. Once all is received, he or she will register your names on the deed along with your new mortgage. You will then receive the keys to your new home! I have worked in the legal field for over a decade before I branched over to mortgage origination. I love helping first time home buyers with the process of buying their first home! If you have any questions, please do not hesitate to call or write. Sarah A. Colucci Mortgage Agent Lic. M14000929 Mortgage Edge, Broker 10680 Direct: (647) 773-4849 Email: sarah.colucci@coluccimortgage.com  If you have high credit card balances, you should probably take the opportunity to explore balance transfers. Usually, a balance transfer will allow you to take advantage of a low interest, introductory offer, if you move your current credit card balance over to another credit card holder.

So, for example, if you're paying 23.999% interest on $10,000, you can move the entire balance over to another credit card holder for, let's say, 1.99%. Usually, introductory offers are for a limited time like nine months, for example, which means you need to make larger monthly payments within that time frame. But, because you will be paying significantly less interest, most of your payments will be going towards principal. Many lenders offer balance transfers, so if you don't have a lot of debt and just want to pay less interest, look into it! Here's a great offer from Bank of Montreal. If, on the other hand, you find yourself struggling with copious amounts of credit card debt that you can't seem to shake, why not explore refinancing your mortgage? Refinancing is an excellent way to consolidate your debt to achieve one low and manageable monthly payment. You can also utilize prepayment privileges within your mortgage contract to increase your mortgage payments and pay significantly more principal in a shorter period of time. If you have questions about debt restructuring, feel free to contact me directly. I would be happy to help you sort through your finances to help achieve a really great solution. Sarah A. Colucci Mortgage Agent Lic. M14000929 Mortgage Edge, Broker. 10680 Direct: (647) 773-4849 Email: sarah.colucci@coluccimortgage.com  It's no secret. The new global health threat called COVID-19 has dampened the global economy and is forcing policy makers to lower their interest rates. Just today, the US Central Bank cut its overnight rate by an unprecedented half a percent. And tomorrow, the Bank of Canada will meet to discuss its overnight lending rate and whether or not rate cuts are warranted.

As the Financial Post reported today, it's likely the Bank of Canada WILL cut its rate given the need to stimulate the economy, however, by how much is still anyone's guess. BOC tends to be conservative and would likely require more time to sort through the situation before making any major changes. Any cut to the overnight lending rate will influence variable rate credit facilities so if the rate goes down, expect to see a lower variable rate mortgage. Are major rate cuts good for the economy? Ultimately, no. When interest rates are low, it entices consumers to borrow more because the cost is cheaper. Although this seems like a good idea, it can pose a problem when interest rates suddenly rise as borrowers can experience "payment shock" and default on their loans. Major insolvencies can then put a heavy strain on the banking system which is also one of the reasons a recession can occur. So, what's actually happening right now with mortgage rates? Mortgage interest rates are dropping as investors flee to the bond market. We say "flee" because the bond market is the safest place during extreme volatility and uncertainty. It's considered a "safe haven" because it has considerably less risk in comparison to the stock market. As a result, bond yields decrease, which pushes mortgage rates down. Again, no one will argue that this is wonderful for prudent mortgage borrowers because they will capitalize on lower interest rates, pay down their mortgages faster and save more money, however, low rates also create much more competition and could bring back the bidding wars which artificially increased property values. Mortgage rates are plummeting day by day, with new mortgage specials here, there and everywhere. Therefore, borrowers should use this time wisely and prioritize their finances which can include refinancing their current mortgage at a lower rate to, let's say, consolidate debt for example, purchasing their first home or making sure they lock in a great rate on their mortgage renewal. Mortgage interest rates can be held for up 120 days or 4 months, which gives borrowers ample time to take advantage of an unprecedented rate environment. And we mustn't forget, that even before the global health threat came to be, real estate was already showing signs of improvement in Toronto and Vancouver. Do you have mortgage questions? Don't hesitate to call or write. Sarah A. Colucci Mortgage Agent, Lic. M14000929 Mortgage Edge, Mortgage Broker 10680 Direct: (647) 773-4849 Email: sarah.colucci@coluccimortgage.com |

By: Sarah ColucciSenior Mortgage Agent, Lic. M14000929 Categories |

- HOME

- MORTGAGE CALCULATORS

- APPLY ONLINE

-

PRODUCTS

- Free House Value Tracker Report

- CASH-BACK MORTGAGE

- BRIDGE FUNDS

- REVERSE MORTGAGES

- SELF-EMPLOYED MORTGAGES

- FIRST-TIME HOME BUYER PRE-APPROVALS >

- MORTGAGE REFINANCE >

- SPOUSAL BUYOUTS

- INVESTMENT PROPERTIES AND RENTALS

- BRUISED CREDIT

- PRE-APPROVALS

- NEWCOMERS

- DEBT CONSOLIDATION

- HOME EQUITY LINE OF CREDIT

- PURCHASE PLUS IMPROVEMENT PROGRAM

- WHY INVEST IN REAL ESTATE

- MORTGAGE RENEWALS >

- SECOND MORTGAGE LOANS

- LESS THAN 20% PROPERTIES

- DOWN PAYMENT

- CONTACT ME

- PRIME RATE CANADA

- CLOSING COSTS

- DOCUMENTS REQUIRED FOR MORTGAGE FINANCING

- MORTGAGE DICTIONARY

- MORTGAGE NEWS

- GOVERNMENT MORTGAGE RULES

- MORTGAGE TIPS

- HOUSE HUNTING CHECKLIST

- APPRAISALS

- FIXED OR VARIABLE RATE?

RSS Feed

RSS Feed GET IN TOUCH WITH SARAH

Let's get started today.

Address411 Queen St.

Newmarket, ON L3Y 2G9 Sarah A. Colucci, Mortgage Agent Lic. M14000929 Sherwood Mortgage Group Licence # 12176 |

TelephoneDirect: 647-773-4849

Email: scolucci@sherwoodmortgagegroup.com |